Rostow stages of economic development are 5 stages through which every must pass through to become developed. These stages are given by an American Economic historian Walter W. Rostow in his book “The Stages of Economic Growth” in 1960. These stages are.

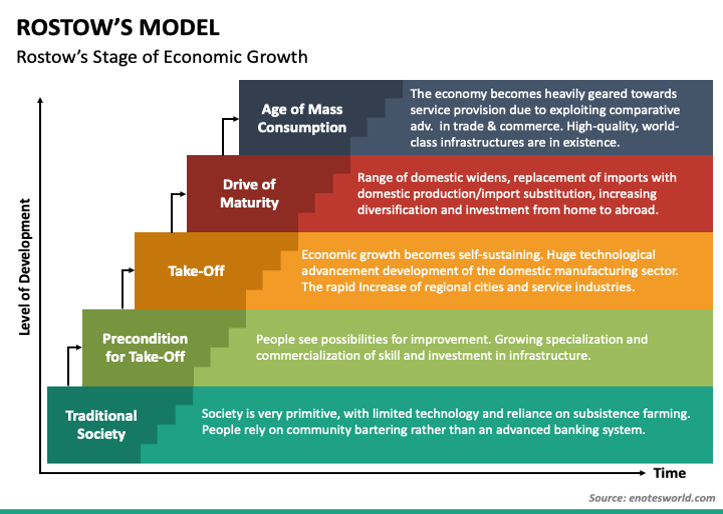

- The traditional society

- The precondition for takeoff

- The takeoff

- The drive to maturity

- The age of high mass consumption

Classical Theories of Economic Development

- Linear Stage Models

- Rostow Stages of Economic Development

- Harrod-Domar Growth Model

- Structural Change Models

- Lewis Model of Economic Development

- Fei-Ranis Two-Sector Model

- International Dependence Model

- Neocolonial Dependence Model

- The False-paradigm Model

- The Dualistic-development Thesis

- Neoclassical Growth Model

- Solow Growth Model

Rostow Stages of Economic Development

1. The Traditional Society

- In their first stage the economies are characterized as agrarian economy in which there is subsistence farming and limited use of technology.

- The agriculture relies heavily on manual labor and traditional methods of production leading to low agriculture productivity and lower income per-capita.

- Due to low per capita income there less investment on healthcare therefore mortality rates were high.

- About more than 75% of the workforce relied on agriculture.

- Investment is less than 5% of GNP and there was limited industrial production.

- This stage is also known as Pre-Newtonian stage due to inadequate knowledge and technology.

- Social system was based on caste and political power was concentrated to few landowners.

2. The Preconditions for Take-off

- During this stage economies start investing on infrastructure such as roads, railways, ports, automobiles and banking.

- People adopt more productive methods in agriculture which lead to surplus output for trading.

- Exports mainly concentrated on primary and semi-finished products. Finished and capital goods are imported.

- Population growth and urbanization also begins. But population growth is greater than output growth, therefore output per capita remains low.

- Investment rate is between 5% to 10% of GNP.

- Birth rates decline due to lower reliance of workers on agriculture which increase their income, leading to lower demand for labor and lower family size is preferred.

- Other sectors like industry, trade and transport start developing but Agri-sector is still dominant sector of the economy.

- The Industrial Revolution in Britain (late 18th century) marks this stage, with the rise of steam engines, canals, and early railways.

3. The Take-off

- This stage is characterized by rapid industrialization and sustained economic growth.

- It is a short period that lasts for about 30 years.

- Manufacturing grows, and productivity increases dramatically. New industries are established and new innovations take place.

- The GDP growth rate is over 5% per annum. Structural transformation occurs from agriculture to industry (share of agriculture in GDP falls significantly).

- Entrepreneurs reinvest their profits which increase investment and reaches over 10% of the GNP.

4. The Derive to Maturity

- In this stage, the economy diversifies into new industries and living standard rises due to lower reliance of laborers on Agri-sector.

- This stage is the outcome of take-off stage. This stage is reached after 40 to 60 years of the take-off stage and lasts for long time period from 50 to 100 years.

- Technological innovation provides a wide range of investment opportunities. There’s greater investment in infrastructure, education, and more complex industries like automobiles, electrical industries and chemical industries.

- Investment rates rise to 10% to 20% of GNP.

5. The Age of High Mass Consumption

- The Age of High Mass Consumption is characterized by a shift from heavy industry to a focus on consumer goods and services.

- Economies in this stage have high levels of consumption of comforts and luxuries and income levels are also very high.

- People have widespread access to goods like automobiles, electronics, and leisure activities. The standard of living is high.

- Governments invest in welfare programs, health systems, and social security to enhance the quality of life.

- The services sector becomes the largest contributor to GDP.

- The rate of investment rises significantly above 20% of GNP.

Conclusion

The United Kingdom was the first country to achieve all five stages, leading the Industrial Revolution. The USA and Western European nations followed. Countries like China and India are considered to be in the “drive to maturity” stage, with rapid industrialization, urbanization, and increasing technological progress.

Criticism of Rostow Stages of Economic Development

- It is not necessary for all countries to pass through the first stage i.e., the traditional society because there are countries like the US, Canada, New Zealand, and Australia that are born free of traditional society, these countries derived pre-condition stage from the Britain which was already advanced.

- There is overlapping in different stages. There are some countries where agriculture sector was continually dominant sector in take-off stage. In countries like New Zealand and Denmark social overhead capital developed during take-off stage.

- This theory neglects the influence of external, global, political, and cultural factors influencing economic development.

Suggestions for further readings

2 Responses