What is Multiple Linear Regression?

The linear regression model shows the linear dependence of one variable on one or more independent variables. A simple linear regression model consists of the linear dependence of one variable on only one independent variable. It is also called a bivariate or two-variable regression model. Such as the dependence of consumption on disposable income.

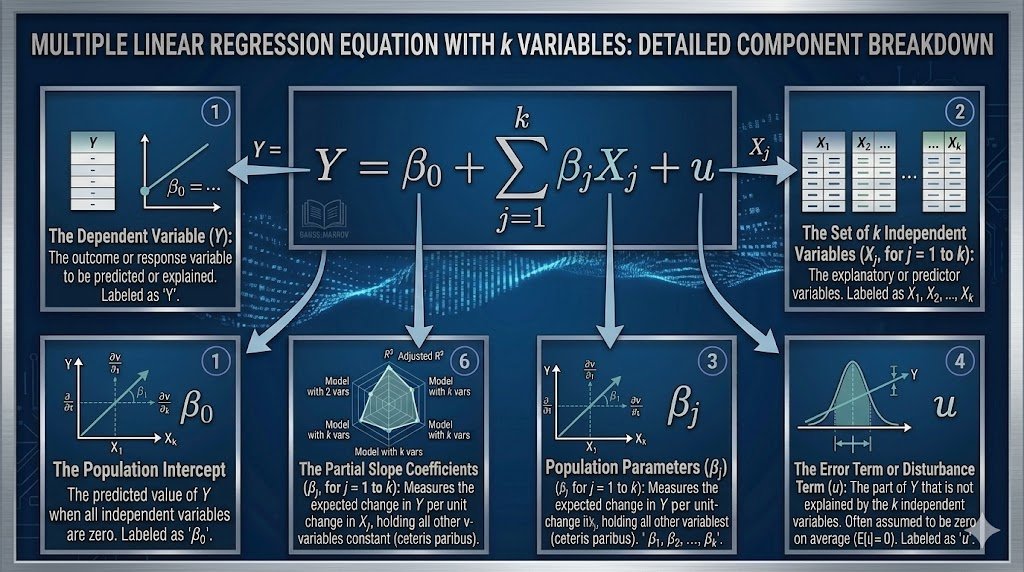

A multiple linear regression model consists of the linear dependence of one variable on two or more independent variables. In other words, in multiple linear regression,, a dependent variable is exprrssed asa linear function of more than one independent variable. It is also called a multivariate regression model. For example, crop yield depends on rainfall, temperature, sunshine, fertilizer, etc. A k-variable multiple linear regression model can be written as:

: Dependent variable

: Dependent variable : Intercept term

: Intercept term : Coefficients of independent variables

: Coefficients of independent variables : Independent variables

: Independent variables : Error term

: Error term

: Dependent variable

: Dependent variable : Intercept term

: Intercept term : Coefficients of independent variables

: Coefficients of independent variables : Independent variables

: Independent variables : Error term

: Error termTo understand multiple linear regression and its interpretation, we consider an example of a 3-variable linear regression model, in which the dependent variable is a linear function of only two explanatory variables. It is written as:

A Numerical Example of Multiple Linear Regression

The following table provides data about monthly sales revenue in USD 1000 (Yi), price index for all products sold in a given month (X1i), and expenditure on advertising in USD 1000 (X2i).

| Obs. | sales | price | advert |

| 1 | 73.2 | 5.69 | 1.3 |

| 2 | 71.8 | 6.49 | 2.9 |

| 3 | 62.4 | 5.63 | 0.8 |

| 4 | 67.4 | 6.22 | 0.7 |

| 5 | 89.3 | 5.02 | 1.5 |

| 6 | 70.3 | 6.41 | 1.3 |

| 7 | 73.2 | 5.85 | 1.8 |

| 8 | 86.1 | 5.41 | 2.4 |

| 9 | 81 | 6.24 | 0.7 |

| 10 | 76.4 | 6.2 | 3 |

| 11 | 76.6 | 5.48 | 2.8 |

| 12 | 82.2 | 6.14 | 2.7 |

Answer the following questions.

- Estimate and interpret the following model:

- Compute and interpret the multiple coefficient of determination and the multiple standard error of estimate.

- Test the significance of regression coefficients and tell whether the signs are according to the underlying theory?

- Predict the sales revenue at means.

Solution

1. Estimate and interpret the following model:

.

The OLS estimates can be obtained by the following formulas.

The following identities can be used to find the values in the above formulas.

| Obs. | Y | X1 | X2 | X1Y | X2Y | X1X2 | X12 | X22 | Y2 |

| 1 | 73.2 | 5.69 | 1.3 | 416.508 | 95.16 | 7.397 | 32.3761 | 1.69 | 5358.24 |

| 2 | 71.8 | 6.49 | 2.9 | 465.982 | 208.22 | 18.821 | 42.1201 | 8.41 | 5155.24 |

| 3 | 62.4 | 5.63 | 0.8 | 351.312 | 49.92 | 4.504 | 31.6969 | 0.64 | 3893.76 |

| 4 | 67.4 | 6.22 | 0.7 | 419.228 | 47.18 | 4.354 | 38.6884 | 0.49 | 4542.76 |

| 5 | 89.3 | 5.02 | 1.5 | 448.286 | 133.95 | 7.53 | 25.2004 | 2.25 | 7974.49 |

| 6 | 70.3 | 6.41 | 1.3 | 450.623 | 91.39 | 8.333 | 41.0881 | 1.69 | 4942.09 |

| 7 | 73.2 | 5.85 | 1.8 | 428.22 | 131.76 | 10.53 | 34.2225 | 3.24 | 5358.24 |

| 8 | 86.1 | 5.41 | 2.4 | 465.801 | 206.64 | 12.984 | 29.2681 | 5.76 | 7413.21 |

| 9 | 81 | 6.24 | 0.7 | 505.44 | 56.7 | 4.368 | 38.9376 | 0.49 | 6561 |

| 10 | 76.4 | 6.2 | 3 | 473.68 | 229.2 | 18.6 | 38.44 | 9 | 5836.96 |

| 11 | 76.6 | 5.48 | 2.8 | 419.768 | 214.48 | 15.344 | 30.0304 | 7.84 | 5867.56 |

| 12 | 82.2 | 6.14 | 2.7 | 504.708 | 221.94 | 16.578 | 37.6996 | 7.29 | 6756.84 |

| ∑ | 909.9 | 70.78 | 21.9 | 5349.56 | 1686.54 | 129.343 | 419.768 | 48.79 | 69660.4 |

| Mean | 75.825 | 5.89833 | 1.825 | 445.796 | 140.545 | 10.7786 | 34.9807 | 4.06583 | 5805.03 |

Plugging these values in OLS formula, we get

Estimated Regression Equation:

2. Compute and interpret the multiple coefficient of determination and the multiple standard error of estimate

Multiple Coefficient of Determination

Formula 1:

Formula 2:

Multiple Standard Error of Estimate

3. Test the significance of regression coefficients and tell whether the signs are according to the underlying theory.

Standard error and t-value of

Standard error and t-value of

4. Predict the sales revenue at mean price and mean advertisement expenditures.

The estimated regression equation is.

Substituting the mean values of  and

and  , that is plugging

, that is plugging  and

and  .

.

Regression Output Results Summary

Interpretation of Regression Results

Interpretation of Coefficients and their significance

The regression results show that if the price index of sold goods increases by 1 unit, then sales revenue will decrease by USD 7.8 thousand, holding the advertising expenditure constant. If the advertising expenditure increases by USD 1000, then sales revenue will increase by USD 3000, holding the price index constant. The intercept value shows that the sales revenue is USD 116.3 thousand if the price index of sold goods and advertising expenditure are zero. It makes no sense that if the price index is zero, then the sales revenue is USD 116.3 thousand, because the sales formula is P*Q; if P = 0, then sales must be zero.

The absolute t-value of is 1.668, which is less than its critical value; therefore, we fail to reject the null hypothesis and conclude that the sales price index has a statistically insignificant effect on sales revenue.

The t-value of is less than its critical value, so we fail to reject the null hypothesis and conclude that advertising expenditure has no statistically significant impact on sales revenue.

According to the underlying theory, the signs of slope coefficients indicate that an increase in sales price will decrease the demand for the good, leading to a decrease in sales revenue. Similarly, more expenditure on advertising leads to more sales revenue, but the impact of both variables on sales revenue is statistically insignificant.

Interpretation of Multiple R2

The R2 value of 0.323 shows that about 32.3% of the variation in sales revenue is explained by the sales price index and advertising expenditure together. While 67.7% of the variation in sales revenue remains unexplained, it is important to consider other factors.

Suggestions for further readings:

MinhajMetricsHub

MinhajMetricsHub

3 Responses