What is Portfolio?

Portfolio is a collection of financial assets owned by an individual or institution, such as stocks, bonds, cash, mutual funds, real estate, commodities, and other investments.

Diversification

Diversification is the process of spreading investments across a variety of assets to reduce overall portfolio risk without sacrificing returns. The portfolio allows for diversifying risk.

Diversification of risk does not mean that there will be an elimination of risk at all. With every asset, there is an attachment of two types of risk: diversifiable risk and undiversifiable risk. Even an optimum portfolio cannot eliminate market risk, but can only reduce or eliminate the diversifiable risk.

Types of Risk

Risk is defined as the range by which an asset’s price will vary on average. Markowitz split risk into two subsequent categories

- Diversifiable Risk or Unsystematic Risk

- Undiversifiable or Systematic Risk

Diversifiable Risk

Diversifiable Risk: It is the internal risk that is specific to a company, industry, or sector. It can be reduced or eliminated through diversification. It is also called unsystematic risk.

Sources of diversifiable risk are the following:

- Business Risk – Internal issues like poor management or operational inefficiencies.

- Competitive Risk – Market share loss due to new competitors or pricing wars.

- Financial Risk – High debt, liquidity problems, or cash flow issues.

- Labor & Strike Risk – Workforce disputes, strikes, or employee dissatisfaction.

Undiversifiable Risk

Undiversifiable Risk: It is the risk that affects the entire market or economy and cannot be eliminated through diversification. It is also called ‘systematic’ or ‘market’ risk.

Sources of Undiversifiable Risk:

- Economic recessions or boom

- Inflation and interest rate changes

- Political instability and government policies

- Natural disasters or global pandemics

Portfolio Management

Portfolio management is the art and science of managing investments through asset allocation, security selection, risk control, and performance evaluation to achieve an investor’s long term financial objectives.

- Asset Allocation: Deciding how to divide the total investment among different asset classes (such as stocks, bonds, real estate, and cash)

- Security Selection: Choosing specific securities (e.g., which stocks or bonds to buy) within each asset class.

- Risk Management: Identifying, measuring, and controlling risks (like market risk, credit risk, or liquidity risk).

- Performance Monitoring: Regularly reviewing the portfolio to assess whether it meets the investor’s goals.

A portfolio manager is a person who understands his client’s investment needs and suggests a suitable investment mix to meet their client’s investment objectives.

Objectives of Portfolio Management

- Capital growth

- Security of principal amount invested

- Liquidity

- Marketability of securities invested in

- Diversification of risk

- Consistent returns

- Tax planning

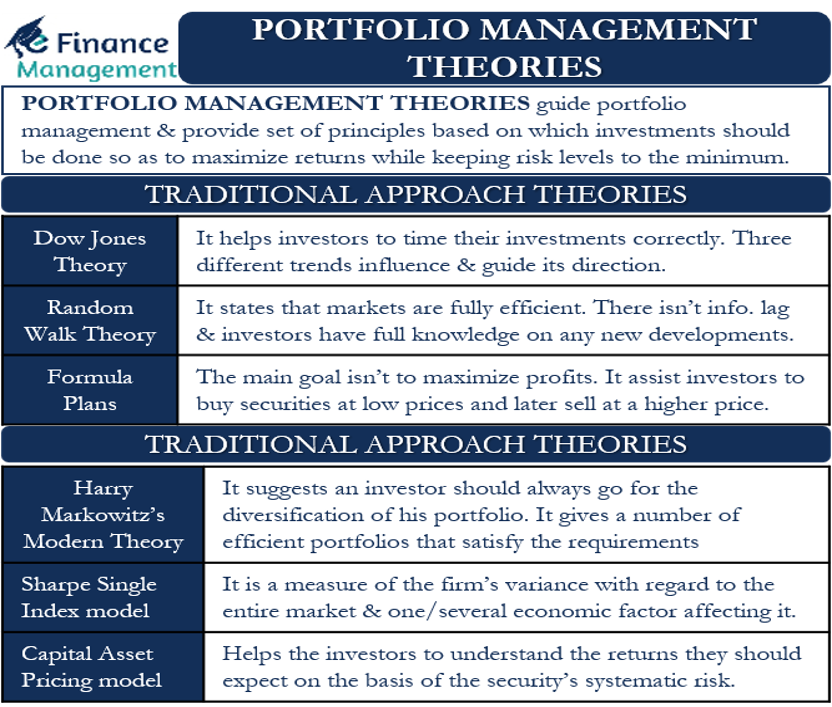

Portfolio Management Theories

Portfolio management theories are the theories that guide portfolio management. They provide a set of principles on the basis of which investments should be made so as to maximize returns while keeping risk levels to a minimum.

There are two approaches to portfolio management theories.

1. Traditional Approach

- Dow Jones Theory

- Random Walk Theory

- Formula Plans

2. Modern Approach

- Harry Markowitz’s Modern Portfolio Theory

- Sharpe Single Index Model

- Capital Asset Pricing Model

Expected Return of a Security

The expected return of a security is the weighted average of all possible returns, where the weights are the probabilities of occurrence of each return. It represents the mean return an investor anticipates earning from a security over a period of time.

| Return (%) | Probability |

| 10 | 0.3 |

| 5 | 0.5 |

| -2 | 0.2 |

Harry Markowitz’s Modern Portfolio Theory

In 1952, an American economist, Harry Markowitz, wrote his dissertation on “Portfolio Selection”, published in the Journal of Finance. In 1990, he won the Nobel Prize in Economic Sciences for Modern Portfolio Theory (MPT). Therefore, he is also known as the father of modern portfolio theory.

MPT is a mathematical method that provides a framework for constructing an optimal portfolio that maximises expected return for a given level of risk or minimises risk for a given level of expected return.

This theory was based on two main concepts:

- Every investor’s goal is to maximise return for any level of risk.

- Risk can be reduced by diversifying a portfolio.

MPT works under the assumption that investors are risk-averse, meaning they prefer a portfolio with less risk for a given level of return. Under this assumption, investors will only take on high-risk investments if they can expect a larger reward.

An Example

Consider an example a “rational investor” is asked to choose between two investments: Investment A and Investment B. Both investments have equal expected rate of return which 6%. However, Investment B is considered twice as volatile as Investment A, meaning its value fluctuates at twice the magnitude of Investment A’s value fluctuations.

MPT suggests that a rational investor will always choose the less volatile asset, in this case Investment A, so long as both investments have equivalent expected return.

Portfolio Risk

MPT is also called the mean-variance model because it uses the mean to calculate expected return and variance (or standard deviation) to calculate risk in a portfolio.

A portfolio’s risk measures the uncertainty or volatility of the portfolio’s return. Overall portfolio risk depends on the variances of each asset and the correlations between each pair of assets. For a portfolio with 2 assets, portfolio risk can be found as

Where ρ12 is the correlation coefficient between assets 1 and 2.

The MPT suggests that the risk of each asset itself contributes very little to overall portfolio risk. Rather, the covariances among the individual assets determine more of the overall portfolio risk. Therefore, investors can reduce individual asset risk by combining a diversified portfolio of assets such that their correlations are low or negative.

Portfolio Return

Portfolio return is the weighted average of the returns of all assets in the portfolio, reflecting the overall gain or loss. If a portfolio contains n assets, the formula is:

Consider an investor holds a portfolio with USD 4,000 invested in Asset Z and USD 1,000 invested in Asset Y. The expected return on Z is 10%, and the expected return on Y is 3%. The expected return of the portfolio is:

Expected Return = [(USD 4,000/USD 5,000) ∗ 10%] + [(USD 1,000/USD 5,000) ∗ 3%] = [0.8 ∗ 10%] + [0.2 ∗ 3%] = 8.6%

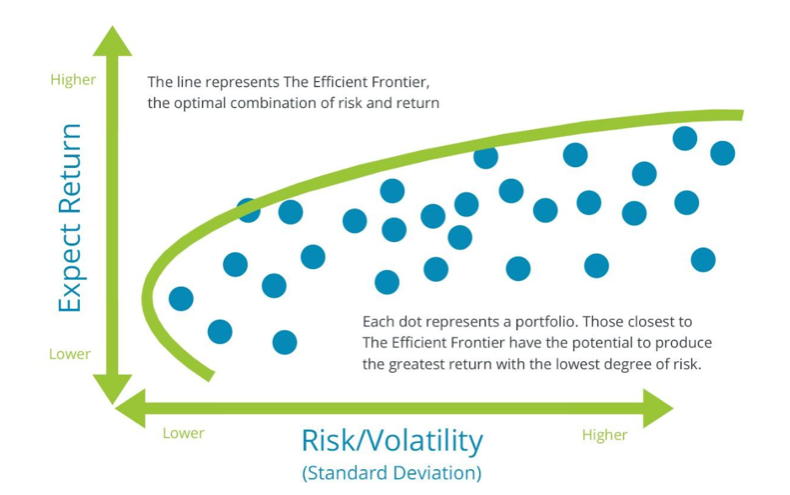

Efficient Frontier

The MPT is helpful to investors to construct an efficient portfolio. An efficient portfolio is one that lies on the efficient frontier, which provides the highest return for a given level of risk, or the lowest risk for a given level of return.

The efficient frontier represents the set of efficient portfolios that offers the highest expected return for a given level of risk, or, conversely, the lowest risk for a given expected return. It is efficient because no other portfolio can provide a better return for the same risk or less risk for the same return.

Each point on this curve corresponds to a portfolio that is ‘efficient’, meaning no other portfolio exists that can provide a higher return for the same risk or a lower risk for the same return. Portfolios below the efficient frontier are considered sub-optimal because they offer lower returns for the same risk, while portfolios above the frontier are unattainable given current assets and market conditions.

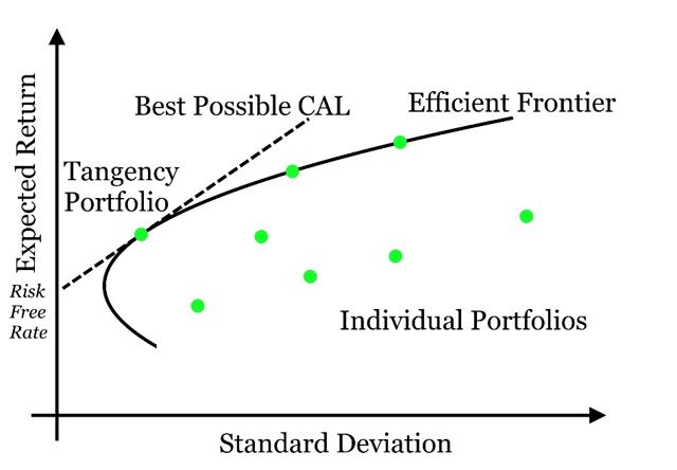

Optimal Portfolio

Although there are various efficient portfolios on the efficient frontier, there is one that is considered optimal. The Optimal Portfolio occurs where the capital allocation line (CAL) intersects with the efficient frontier. The CAL demonstrates the risk-return trade-off for all investment assets, considering the presence of a risk-free asset.

The risk-free rate of return refers to the rate of return an investor expects to earn on an asset with zero risk. All assets carry some degree of risk; therefore, assets that generally have low default risks and fixed returns are considered risk-free. An example of a risk-free asset is a 3-month government Treasury bill.

Additionally, the slope of the CAL, known as the Sharpe ratio, indicates the risk-adjusted returns of an asset or portfolio. The highest Sharpe ratio occurs at the tangency of the CAL and the efficient frontier, which is the optimal portfolio. This point of tangency identifies the optimal risky portfolio, which offers the best risk-return trade-off.

The optimal portfolio occurs where the capital allocation line (CAL) becomes tangent to the efficient frontier.

v

MinhajMetricsHub

MinhajMetricsHub