GDP has four types of expenditure such as consumption, investment, government expenditure and net exports. We call this expenditure as components of GDP. Each unit of money spend in the economy fall into one of these 4 components of GDP. Before studying components of GDP, we must know what GDP is.

What is GDP?

In the previous blog post, we discussed national income and its various concepts. All these concepts of national income are closely related and essentially measure the same economic activity from different perspectives, with some necessary adjustments. However, GDP is the most widely used measure of aggregate economic activity. It is commonly used to compare economic progress across countries and over time.

GDP measures the total domestic output of a country during a specific period, usually one year or one quarter. GDP stands for Gross Domestic Product.

- Gross: The market value of all final goods and services is measured without deducting depreciation of fixed capital.

- Domestic: All goods and services produced within the geographical boundaries of a country are included in GDP, regardless of the nationality of the producers.

- Product: Only the market value of currently produced final goods and services is included in a country’s GDP.

To deeply understand GDP, we define it clearly here,

Gross domestic product (GDP) is the total market value of all final goods and services produced within a country in a given period of time.

“GDP Is the Market Value . . .”

GDP is a monetary measure of output produced. It is calculated by adding market value of all the goods and services produced. Market value of a good or service can be calculated by multiplying physical output with price per unit.

For example, if the price of 1 kg apple is RS.100, then the market value of 50 kg of apples would be 50×100=”RS.” 5000. If the price of one dozen of orange is RS.150, then the market value of 100 dozens of oranges would be 100×150=RS.15000. Adding the market value of apples and oranges we get GDP=5000+15000=RS.20,000.

Two types of market prices (value)

- Current market price is the price level currently prevailing in the economy. It is used to measure the nominal GDP.

- Constant prices is the price level of some base year. It is used to measure the real GDP.

If there are n goods and services are produced in the country, then

GDP = P1 × Q1 + P2 × Q2 + … + Pn × Qn

- P1, …, Pn are prices of n goods

- Q1, …, Qn are quantities of n goods produced

“. . . of All . . .”

GDP tries to be comprehensive. It includes all items produced in the economy and sold legally in markets. Some goods and services are not sold at marketplace and therefor do not have market price such as homemakers’ services, output grown for their own use, unreported output from illegal activities such as sale of narcotics, drugs, gambling etc. These are not included in the GDP.

“. . . Final . . .”

GDP includes only the value of final goods because the value of intermediate goods is already included in the prices of the final goods. Final goods are those goods which are purchased for final use and not for resale or further processing. Intermediate goods are those goods which are purchased for further processing or for resale. The sale of intermediate goods is excluded from GDP because the value of final goods includes the value of all intermediate goods.

For example, an iPad is a final good, but an apple chip inside it is an intermediate good. Similarly, tire is an intermediate good while car is a final good.

Double counting occurs when intermediate goods are counted along with final goods in GDP calculation. It results in overestimation of GDP. It can be avoided by:

- Include only the value of final goods and exclude intermediate goods.

- Add value added at each stage of production, not total sales.

“. . . Goods and Services . . .”

GDP includes both tangible goods (food, clothing, cars, electronics and other) and intangible services (haircuts, housecleaning, doctor visits and others).

“. . .Produced . . .”

GDP includes only those goods and services which are produced in a current year. Goods produced in previous year are not included in GDP. For example, a used car isn’t part of GDP. It was part of GDP in the year in which it was produced.

“. . . Within a Country . . .”

GDP measures the value of production within the geographic boundaries of a country. When a Pakistani citizen works temporarily in the United States, her production counts toward U.S GDP. When an American citizen owns a factory in Pakistan, the production at her factory is included in Pakistan`s GDP). Thus, items are included in a nation’s GDP if they are produced domestically, regardless of the nationality of the producer.

“. . . In a Given Period of Time.”

GDP measures the value of production that takes place within a specific interval of time usually, a year or a quarter.

Components of GDP

On one side GDP measures total domestic output, on the other side it also measures total expenditure made on this output. now in a domestic economy there are four types of expenses on GDP. These are:

- Consumption expenditure

- Investment expenditure

- Government Expenditure

- Net Exports

Thus,

GDP (Y) = C + I + G + NX

In fact, each dollar (or rupee) of expenditure on GDP is placed into one of these four components of GDP. Therefore, above equation is an identity—an equation that must be true because of how the variables in the equation are defined.

When we add all components of expenditure such as consumption, investment, government expenses and net exports made by all households, firms, government and foreign sector we call it expenditure approach to measure GDP.

Now we define each component of expenditure in detail.

Consumption Expenditure (C)

Consumption expenditure refers to the spending of all households on consumer goods in a year except for purchases of new housing. This is the largest component of GDP. Consumer goods include:

- Durable goods: That last for relatively longer period of time such as automobiles, furniture, household appliances etc.

- Nondurable goods: That are used up fairly quickly such as food, clothing, gasoline etc.

- Services are nontangible items that we buy such as expenditures for doctors, lawyers, and educational institutions.

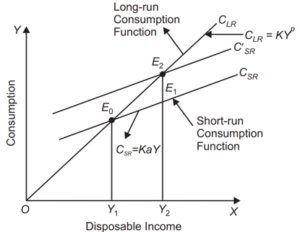

Consumption expenditure depends on disposable income of households, the more income we have the more we can spend on consumer goods and services. The relationship between consumption and disposable income is represented by the consumption function written as:

C = f(Y)

A linear consumption function can be written as:

C = C0 + cY

Investment Expenditure (I)

Investment expenditure refers to the spending of firms on the purchase of new capital goods that will be used in the future to produce more goods and services such as housing, plants, equipment, and inventory in a year. Investment is the sum of three types of investment:

- Business fixed investment: It refers to the investment in the fixed capital such as buildings, machines, tools and equipment that firms buy for use in further production of goods and services.

- Residential investment It refers to the expenditure make on constructing or buying new houses or apartments for the purpose of living or renting out to others.

- Inventory investment is the increase in firm`s inventory of goods. Inventories are the goods that firms produce now but intend to sell later. Inventories are counted as capital because they produce value in the future. Inventories may include raw material, semi-finished goods and finished goods.

Government Expenditure (G)

Government expenditures are the purchases of goods and services by the federal, state, and local government to provide public goods and services. These services include defense, law and order, infrastructure, health and education etc. Govt. transfer payments are not included in GDP because they are not made in exchange for a currently produced good or service.

Net Exports (NX)

Net exports is the difference between exports and imports.

- Exports (X) are goods and services produced domestically by purchased by foreigners. Exports are included in a country`s GDP because these represent domestic production.

- Imports (M) are goods and services produced in foreign country but purchased by domestic residents. Imports are excluded from country`s GDP because these represent foreign production.

Thus,

NX = X − M

- Net Exports are positive if exports are greater than imports.

- Net exports are negative if imports are greater than exports.

- Net exports are zero if exports and imports are equal.

Solved Example

| Component | Value (in Million) |

| Personal Consumption Expenditure (C) | 6,500 |

| State Government Consumption and Investment Expenditure (G) | 500 |

| Central Government Consumption and Investment Expenditure (G) | 2,000 |

| Change in Business Inventories (I) | 100 |

| Gross Private Domestic Fixed Investment (I) | 1,200 |

| Exports (X) | 900 |

| Imports (M) | 1,200 |

Answer

GDP = C + I + G + X − M

Where:

C = Personal Consumption Expenditure

G = Government Consumption and Investment Expenditure (Central + State)

I = Gross Private Domestic Fixed Investment + Change in Inventories

X = Exports

M = Imports

GDP = 6,500 + 1,200 + 100 + 500 + 2,000 + 900 − 1,200

= 10,000

Solve Yourself: Example 1

Given the data in table below, find GDP by expenditure method.

| Component | Value in Billion Rs. |

| Private Final Consumption Expenditure | 290 |

| Government’s Final Consumption Expenditure | 50 |

| Gross Domestic Fixed Capital Formation | 105 |

| Increase in Inventories | 15 |

| Net Exports | -5 |

Solve Yourself: Example 2

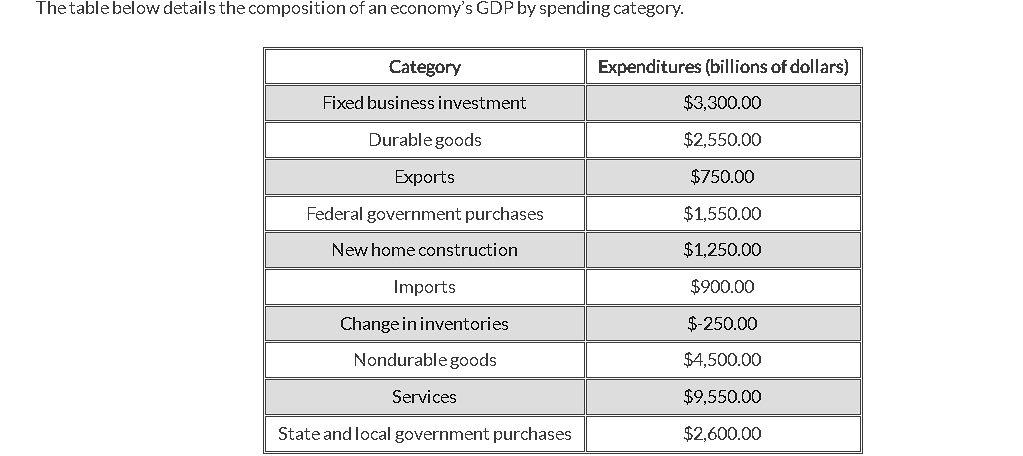

Given the data in below table about components of GDP, Calculate GDP by expenditure method.

Test Your Understanding!

An American buys a pair of shoes made in Italy. how do the U.S. national income accounts treat the transaction?

- Net exports and GDP both rise.

- Net exports and GDP both fall

- Net exports fall, while GDP does not change.

- Net exports do not change, while GDP rises.

Suggestions for further readings

MinhajMetricsHub

MinhajMetricsHub

3 Responses