Measurement of National Income

In the post National Income and Its various Concepts, we define national income as

National Income is the sum of income earned by all factors like land, labor, capital and entrepreneur in form of rent, wages, interest and profit in a year.

Alfred Marshall in his book “Principles of Economics” in 1890 defines NI as “

NI is the sum of all physical goods produced, and services provided by utilizing all its natural resources with the help of capital and labor. Net income from abroad is also included.”

It can also be defined as the total market value of all final goods and services produced in the economy in a year. Thus, national income simultaneously represents three things.

- Total market value of all goods and services produced.

- Total income received by all individuals such as firms and households.

- Total expenditure made on all goods and services produced

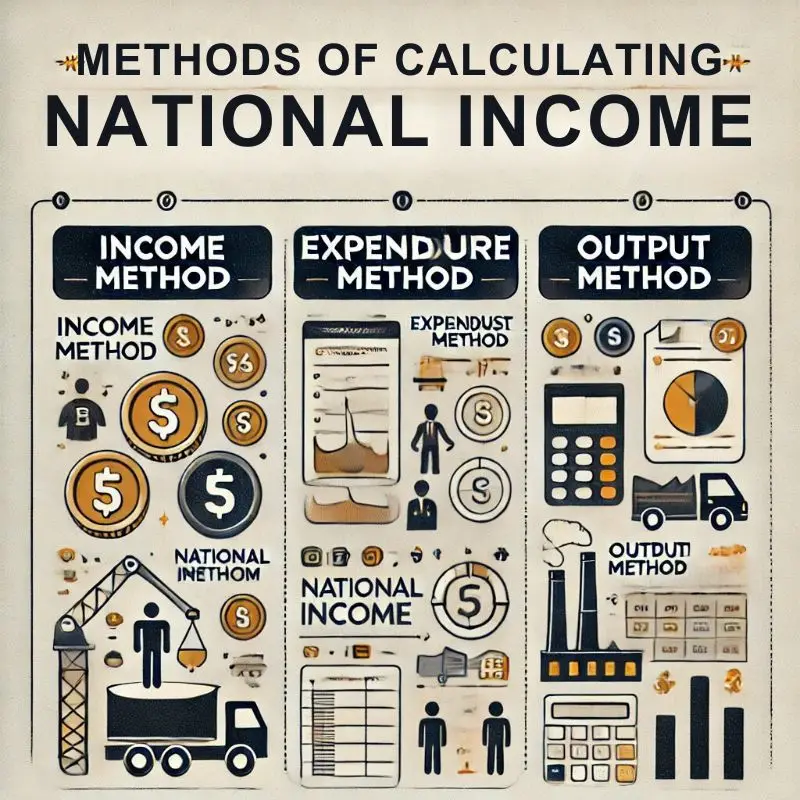

Therefore, there are 3 methods for measurement of National Income. These are:

- Output Approach

- Agriculture

- Industrial

- Services

- Income Approach

- Compensations of Employees

- Rent and Royalty

- Interest

- Profit

- Mixed Income

- Expenditure Approach

- Consumption

- Investment

- Government

- Net Exports

Now we explain each measure in detail

Output or Value-Added Approach

This approach measures national income by adding up the total market value of all final goods and services or value added at each stage of production. This approach divides the economy into three main sectors such as:

- Primary sector (agriculture, mining, fishing, forestry)

- Secondary sector (manufacturing such as textile, cement, automobile, electronics, sugar, steel)

- Tertiary or services sector (banking, education, healthcare, transport, tourism)

Formula

Y = P1 × Q1 + P2 × Q2 + … + Pn × Qn

Precautions

- Only final goods should be included

- Only current output is included

- Production for self-consumption should also be included

- Services of housewives are not included

It is necessary to explain added value method here

As an example, See Value Added GDP Table to calculate GDP using this method

| Stage of Production | Value of Output (Rs. /year) | Value of Intermediate Inputs (Rs. /year) | Value Added (Rs. /year) |

| Farmer (Wheat) | 100 | 0 | 100 |

| Miller (Flour) | 180 | 100 | 80 |

| Baker (Bread) | 260 | 180 | 80 |

| Retailer (Final Sale) | 300 | 260 | 40 |

| GDP (Sum of Value Added) | — | — | 300 Rs./year |

Double Counting

Double counting occurs when intermediate goods are counted along with final goods in GDP calculation. It results in overestimation of national income.

How to avoid double counting

There are two alternative ways to avoid double counting

- Sum value added at each stage of production only

- Count only the value of final output

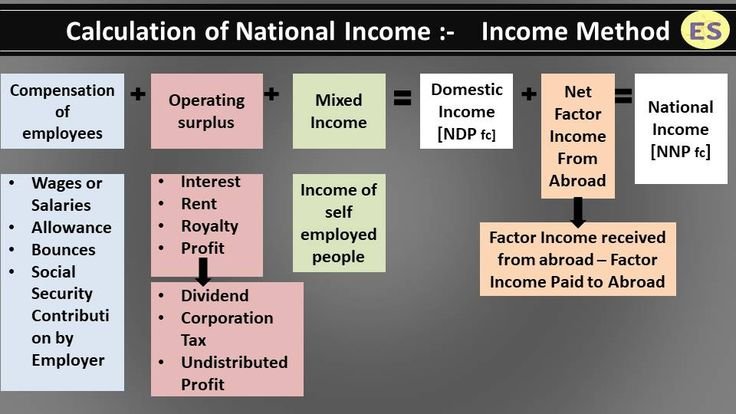

Income Approach

Under the Income Method, national income is obtained by summing up all incomes earned by the people by providing their own services (labour) and the services of their property such as land and capital. It includes the following components:

- Compensation of employees

- Wages and salaries in cash

- Wages and salaries in kind

- Employers’ contribution to social security schemes

- Rent and royalty

- Interest

- Profits

- Dividends

- Undistributed profits

- Corporate income tax

- Mixed income of the self-employed including wages, rent, interest and profit

Formula

Y = R + W + i + Π

Precautions

- Transfer payments are not included

- Money earned from illegal sources not included

- Windfall gains not included

- Sale of second-hand goods are not included

Expenditure Approach

Expenditure approach measures national income by adding up all the spending on final goods and services during a given period by households, firms, government, and foreigners. It is the sum of consumption, investment, government purchases and net exports.

Formula

GDP (Y) = C + I + G + NX

Consumption Expenditure (C)

Consumption expenditure refers to the spending of all households on consumer goods in a year except for purchases of new housing. This is the largest component of GDP. Consumer goods include durable goods, nondurable goods and services.

Consumption expenditure is directly related to disposable income of the consumer. This relationship iis represented by the consumption function.

C = f(Y)

A linear consumption function can be written as:

C = C0 + cY

Investment Expenditure (I)

Investment expenditure refers to the spending of firms on the purchase of new capital goods that will be used in the future to produce more goods and services such as housing, plants, equipment, and inventory in a year. Investment is the sum of three types of investment:

- Business fixed investment: It refers to the investment in the fixed capital such as buildings, machines, tools and equipment.

- Residential investment It refers to the expenditure make on constructing or buying new houses or apartments for the purpose of living or renting out to others.

- Inventory investment: It refers to the increase in firm`s inventory of goods. Inventories may include raw material, semi-finished goods and finished goods.

Government Expenditure (G)

Government expenditures are the purchases of goods and services by the federal, state, and local government to provide public goods and services. These services include defense, law and order, infrastructure, health and education etc. Govt. transfer payments are not included in GDP because they are not made in exchange for a currently produced good or service.

Net Exports (NX)

Net exports is the difference between exports and imports.

- Exports (X) are foreign spending on domestic production. Exports are included in a country`s GDP.

- Imports (M) are domestic spending on foreign production. Imports are excluded from country`s GDP.

Thus,

NX = X − M

- Net Exports are positive if exports are greater than imports.

- Net exports are negative if imports are greater than exports.

- Net exports are zero if exports and imports are equal.

Suggestions for further readings

MinhajMetricsHub

MinhajMetricsHub

One Response